A shot in the arm: Something that has a sudden and positive effect on something, providing encouragement and new activity.

— Cambridge Dictionary

NGF President and CEO Joe Beditz

I can’t think of a more appropriate description of the year 2020 and its effect on golf, can you? There hasn’t been this much optimism and new activity in the golf business since the turn of the century – I almost forgot what it felt like.

I can’t think of a more appropriate description of the year 2020 and its effect on golf, can you? There hasn’t been this much optimism and new activity in the golf business since the turn of the century – I almost forgot what it felt like.

Happy to tell you we’ve wrapped up our 2020 research and begin the reporting of our findings starting with this issue of Fortnight – now the official name of this bi-weekly insights newsletter that many in and around the golf industry have been receiving over the past nine months. Fortnight will serve as NGF’s new primary channel of communication with anyone and everyone who works in the golf business. If you know someone who should be on the distribution list, please forward this to them.

Down to business. We’ve got a lot to discuss — too much for a single message, in fact, so we’re going to divide this “Year in Review” into three parts. This post will provide a few topline numbers on golfers, rounds and course supply. In a forthcoming message, we’ll dig into golf participation and provide details on who came into the game, who left and how some important customer groups fared. Finally, we’ll devote the third issue in the series to supply, sharing insights on golf course openings, closings, renovations and an examination of the trend toward market equilibrium.

For readers who are NGF members, you don’t have to wait. Our full report is available here. Yep, another new name, The Graffis Report, which is what we’ll be calling NGF’s annual year in review – a nod to our founders, Herb and Joe Graffis, who established NGF 85 years ago as the first golf business research, education and trade organization.

Coming into 2020, there was plenty of optimism for the U.S. golf industry, thanks to stable green grass participation and significant growth of engagement away from the course. Then the world was struck by the coronavirus pandemic and golf, like most other businesses, took a huge hit. But spring shutdowns gave way to an unprecedented summer and fall in terms of play, golfer introductions and reintroductions, and robust, late-season spending. As we look back on an astonishing year, several things stand out:

- 14% year-over-year increase in rounds despite March/April course shutdowns

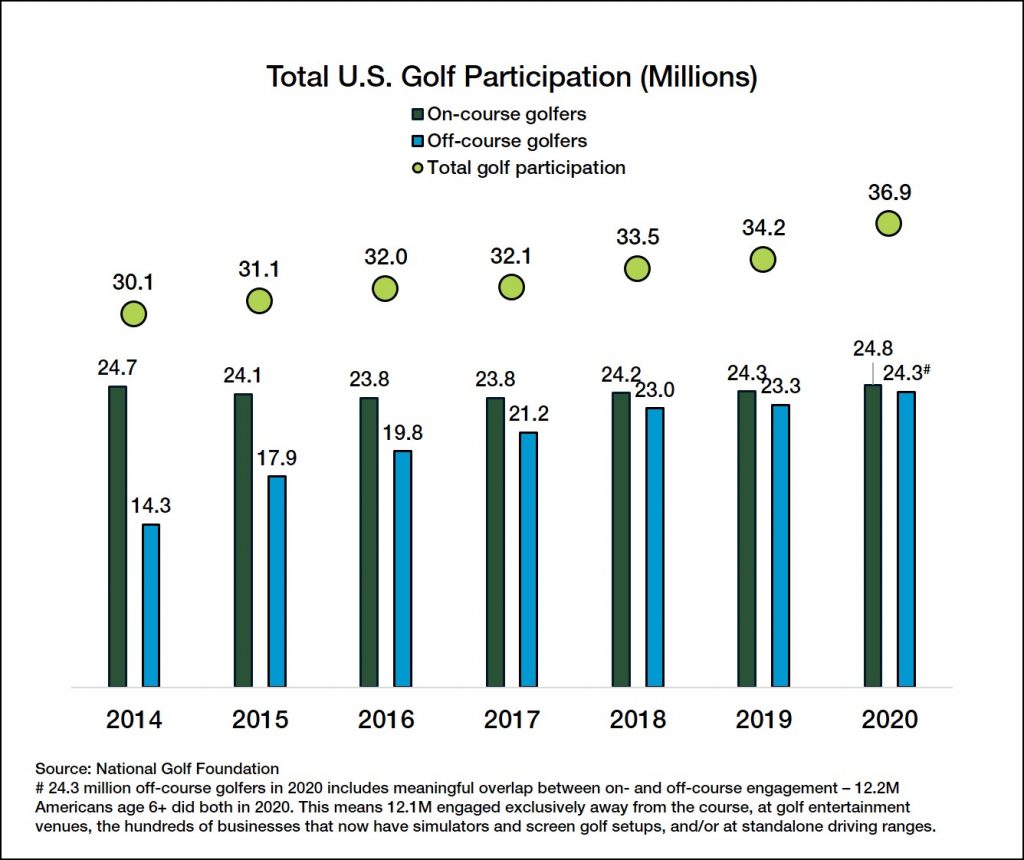

- Total golf participation (on/off-course combined) up 8% Y.O.Y. to 36.9 million participants

- Net gain of 500K on-course golfers, the largest lift in 17 years, up to 24.8M

- An increasing number of interested green grass prospects, up 10% Y.O.Y.

- Significant decrease in the number of course closures as the financial health of facilities nationwide has improved

Surges in play got the most attention in 2020, and rightfully so. Consider that the average weather-related fluctuation is +/- 2%-3% in a typical year and only once in the past two decades was there a 5% Y.O.Y. increase. The 14% jump means that, even with the loss of 20 million spring rounds, the net gain over 2019 was in the neighborhood of 60 million rounds, putting the industry around 500M in total. Heightened demand was particularly evident from June through year’s end, when approximately 75M more rounds were played than the same stretch in 2019.

When we began tracking off-course forms of golf some years back, it was to better quantify the game’s broader consumer base and footprint. This goes well beyond Topgolf – to other golf entertainment venues, and the hundreds of businesses that now have simulators and screen golf setups, plus the good old standalone driving ranges, which believe it or not still outnumber Costco warehouses. Today, almost as many people engage with off-course forms of golf as do traditional “green-grass,” with considerable overlap between the two. Over the past five years, the overall golf consumer pool has risen 19% to 36.9M – including now 12.1M Americans who only hit golf balls with golf clubs somewhere away from the course.

Meanwhile, the number of active, on-course golfers in the U.S. grew by half a million in 2020, up to 24.8 million. It was the most significant Y.O.Y. net increase since 2003, thanks to a record inflow of beginning and returning players (6.2M of them, which is 27% higher than the year before and almost enough to populate Los Angeles and Houston). The net gain could have been even greater, but 2020 was an extraordinary year in more ways than one. Last year 5.7M people stepped away from the game, a 19% increase in outflow versus the year before. The incremental loss was marked by virus anxieties, financial hardships and parenting challenges, and the cancellation of thousands of charity and/or corporate events that draw in “occasional” golfers. Lucky for us, the recently-lapsed participants in 2020 show significantly more interest in returning compared to recently-lapsed in years past.

Speaking of interest, golf’s pipeline of green grass prospects, which we refer to more clinically as “latent demand,” has never been bigger. The number of Americans who didn’t play on a course in the past year but suggest they’re “very interested” in doing so now rose to 17M in 2020 – a 10% increase from the year before and up more than 40% since 2015. As interest continues to swell, there’s been a concomitant rise in the number of beginners, which this year hit an all-time high.

On the supply side, the number of golf course closures dropped significantly (-31%) compared to prior year. NGF recorded a total of 193 18-hole equivalent closures in 2020, about 1.3% of total supply. Demand for land to develop into residential and commercial real estate projects continues to fuel the supply correction in golf.

At the same time, fewer than 8% of the nation’s 14,000+ facilities report that they are in poor financial shape, down from 25% in 2016. Markets are always adjusting, but last year’s downswing in closures and improvements in facility financial health could signal the beginning of the end of golf’s ongoing demand/supply correction, which has lingered for 15 years.